Cách chuẩn bị tài chính cho đầu tư EB-5 trong khi đang làm việc theo visa H-1B

30th Tháng Một, 2024

Trong hướng dẫn này do Vrishin từ CapitalWe và AIIA đồng tác giả, chúng tôi đã tìm hiểu các phương pháp khác nhau mà các nhà đầu tư tiềm năng theo chương trình EB-5 đang sở hữu visa H1-B có thể chuẩn bị tốt nhất cho khoản đầu tư của mình trong tương lai.

Written by Vrishin Subramaniam

For many young immigrant professionals in the United States, the H-1B visa system presents a myriad of challenges and uncertainties. As a financial planner specializing in this group, I frequently witness their anxieties and frustrations stemming from the unpredictability of their immigration and employment status. If they want to change jobs or lose their jobs unexpectedly, they have to find another employer who can sponsor them and file a new H-1B petition, which can be costly and time-consuming. Sometimes, they may have to stay in low-paying or abusive workplaces just to keep their visa status. They also have to deal with the lottery system, the cap on visas, the frequent policy changes, and the potential fraud and abuse by some employers and intermediaries. Moreover, they may not be able to bring their family members who are not eligible for an H-4 visa, such as adult children and elderly parents, which can result in family separation and emotional distress.

For the average H-1B holder, one petition filing can secure green cards for the investor, their spouse, and any children born outside the U.S. Preparation for filing includes securing $800,000 for the investment, an additional $50,000-$80,000 in administrative and professional service costs, and ensuring all funds are well-documented by official sources. An EB-5 project typically doesn’t repay investors until after six to seven years and that too is an “at risk” investment. For this reason, I always recommend that immigrant investors maintain a financial safety net before making this investment.

For H-1B holders seeking permanent residence in the U.S, the EB-5 visa places no conditions on applying, making it ideal for those who wish to avoid backlogs in the EB-1 and EB-2 categories. Petitioners need not know English, hold any type of special honors, degrees, work sponsorships, or have any outstanding abilities to apply. The only conditions required are a whole, sustained investment in a commercial enterprise, ten jobs which are generated through your investment, and a legal source of funds for the investor and their family.

In this blog below I detail some of the common methods my clients and other H1B holders typically finance their investments and what you can do now to start preparing for this investment.

To navigate these financial demands, H-1B holders typically utilize the following options to fund their EB-5 Investment

- Savings: High-earning professionals living in low-cost areas can accumulate substantial savings through diligent budgeting and disciplined spending habits.

- Retirement Accounts: Individuals with sizable 401(k) balances may be able to borrow against these funds through a 401(k) loan, avoiding early withdrawal penalties and preserving retirement savings.

- Home Equity: Homeowners with significant equity can potentially secure a home equity line of credit (HELOC) to finance their EB-5 investment.

- Taxable Brokerage Accounts: Investors with substantial holdings in stocks or bonds can consider a securities-backed line of credit (SB-LOC) to leverage their assets.

- Funds from Home Country: Sale of property or other assets in the investor’s home country can provide the necessary capital as long as there is formal source documentation available.

- Gifts from Family and Friends: Documented gifts from family or friends can contribute to the investment funds.

- Loans: USCIS permits EB-5 investments funded through loans, provided the investor assumes sole responsibility for the debt and secures it with personal assets rather than those of the investment enterprise. (Unsecured loans are an option as well but it can be very tricky to get large unsecured loans.)

Preparing for the Future: A Proactive Approach

To effectively prepare for an EB-5 investment, H-1B holders should adopt a proactive approach:

Start with getting clear on your goals: Defining what is important to you will help provide clarity on what you need to do with your money. E.g. If staying in the country in the long term is more important than owning a home (in the short term) then you need to save into different accounts than buying real estate.

One clear step: Sit down with a piece of paper and write down what all you want to achieve in 1, 3 and 5 years from now. Reorder these from most important to least important.

Automate savings + Conscious spending: I hate the word “budget” since it has a negative connotation, so I instead recommend that people pay more attention to their spending. You need to automate money movement such that each paycheck you send money into a savings/investment account and spend the rest in a manner that aligns with your values.

One clear step: Start before you are ready. Set up a recurring, automated transfer of $100 from your checking account to your savings/investment account each paycheck cycle (biweekly or monthly). You can then adjust this amount as needed.

Spend more money (on self-development): This may seem counterintuitive, but you need to spend more on education and skill development. We as immigrants don’t do this enough and it is holding back your ability to exponentially increase income (especially lack of soft skills).

You are in a different country and the rules are different, so you need to adapt accordingly.

One clear step: Review your most recent performance review, or set up some time with your manager to ask them what you can be doing better or what soft skills would make you invaluable for the team.

Think long-term + Invest wisely: Realize that it is not a sprint but a marathon. You are going to have a much better result by not trying to get a better-than-average return percentage, but saving a better than average savings percentage.

One clear step: Read any or all of the following books:

“The Little Book of Common Sense Investing” by Jack Bogle

“The Psychology of Money” by Morgan Housel

“The Millionaire Next Door” by Thomas J. Stanley

Read up about the Bogleheads portfolio.

Working with a professional: A CPA is good to have, but I also recommend working with a financial planner who is able to guide your finances keeping in mind your visa challenges and goals.

One clear step: Reach out for a free consultation! I work with immigrants on an H1b who don’t want their job and finances to control their life and immigration. I can help you plan for big purchases like the EB-5. Here is a link to book time.

The EB-5 visa is a very common method for H-1B holders to start their transition into permanent residency in the United States. However, transitioning into this visa requires careful financial preparation and due diligence. To learn more about the EB-5 visa, how the program works, and to learn more about what you need to get started, visit the American Immigrant Investor Alliance’s resource library for prospective EB-5 investors.

Danh bạ các chuyên gia

AIIA đã tuyển chọn một danh sách các chuyên gia hàng đầu, bao gồm luật sư, chuyên gia đầu tư và người viết kế hoạch kinh doanh, để hỗ trợ tất cả các bên liên quan đến chương trình EB-5.

Xem Danh bạ Chuyên giaBài viết liên quan

Chuỗi bài viết về Đạo luật Tự do Thông tin (FOIA) của AIIA: Số liệu thống kê cập nhật về hồ sơ I-526E tháng 7 năm 2025

Hiệp hội Đầu tư Nước ngoài Hoa Kỳ (AIIA) gửi ý kiến đóng góp về Dự thảo Quy định (NPRM) của Sở Di trú và Nhập tịch Hoa Kỳ (USCIS) liên quan đến quy định cập nhật về lệ phí EB-5

Chúng tôi xin chúc mừng Thượng nghị sĩ Gallego về dự luật mới tận dụng Chương trình EB-5 để xây dựng nhà ở giá rẻ.

Chúng tôi đã thắng kiện vụ kiện về việc tăng phí EB-5.

Hãy để lại bình luận của bạn

Phản hồi (1)

Danh bạ các chuyên gia

AIIA đã tuyển chọn một danh sách các chuyên gia hàng đầu, bao gồm luật sư, chuyên gia đầu tư và người viết kế hoạch kinh doanh, để hỗ trợ tất cả các bên liên quan đến chương trình EB-5.

Xem Danh bạ Chuyên giaBài viết liên quan

Chuỗi bài viết về Đạo luật Tự do Thông tin (FOIA) của AIIA: Số liệu thống kê cập nhật về hồ sơ I-526E tháng 7 năm 2025

Hiệp hội Đầu tư Nước ngoài Hoa Kỳ (AIIA) gửi ý kiến đóng góp về Dự thảo Quy định (NPRM) của Sở Di trú và Nhập tịch Hoa Kỳ (USCIS) liên quan đến quy định cập nhật về lệ phí EB-5

Chúng tôi xin chúc mừng Thượng nghị sĩ Gallego về dự luật mới tận dụng Chương trình EB-5 để xây dựng nhà ở giá rẻ.

Chúng tôi đã thắng kiện vụ kiện về việc tăng phí EB-5.

Cập nhật thông tin mới nhất từ AIIA

Đăng ký nhận bản tin của chúng tôi để cập nhật thông tin mới nhất về chương trình EB-5.

Bằng cách đăng ký, bạn đồng ý với Chính sách Bảo mật của chúng tôi và đồng ý nhận các cập nhật từ công ty chúng tôi.

Nguồn tài liệu được khuyến nghị

Cách tìm một luật sư giỏi về tranh tụng EB-5

Chọn một luật sư có kinh nghiệm về EB-5 và tranh tụng, người có tổ chức, chú trọng đến chi tiết và tránh đưa ra các cam kết. Bạn có thể cần một...

Đọc thêm

Vấn đề nan giải về việc tái triển khai

Vụ kiện về việc tái đầu tư phát sinh khi các nhà quản lý NCE tái đầu tư vốn EB-5 mà không có sự đánh giá thận trọng, khiến nhà đầu tư phải đối mặt với rủi ro không cần thiết mặc dù có các điều khoản hợp đồng rộng rãi...

Đọc thêm

“Quan hệ trực tiếp” trong vụ kiện EB-5

Các nhà phát hành EB-5 thường thiết kế các cấu trúc phức tạp và mối quan hệ “privity” hẹp để làm cho việc khởi kiện trở nên khó khăn, buộc các nhà đầu tư phải đối mặt với những thách thức lớn và...

Đọc thêmBài viết mới nhất trên blog

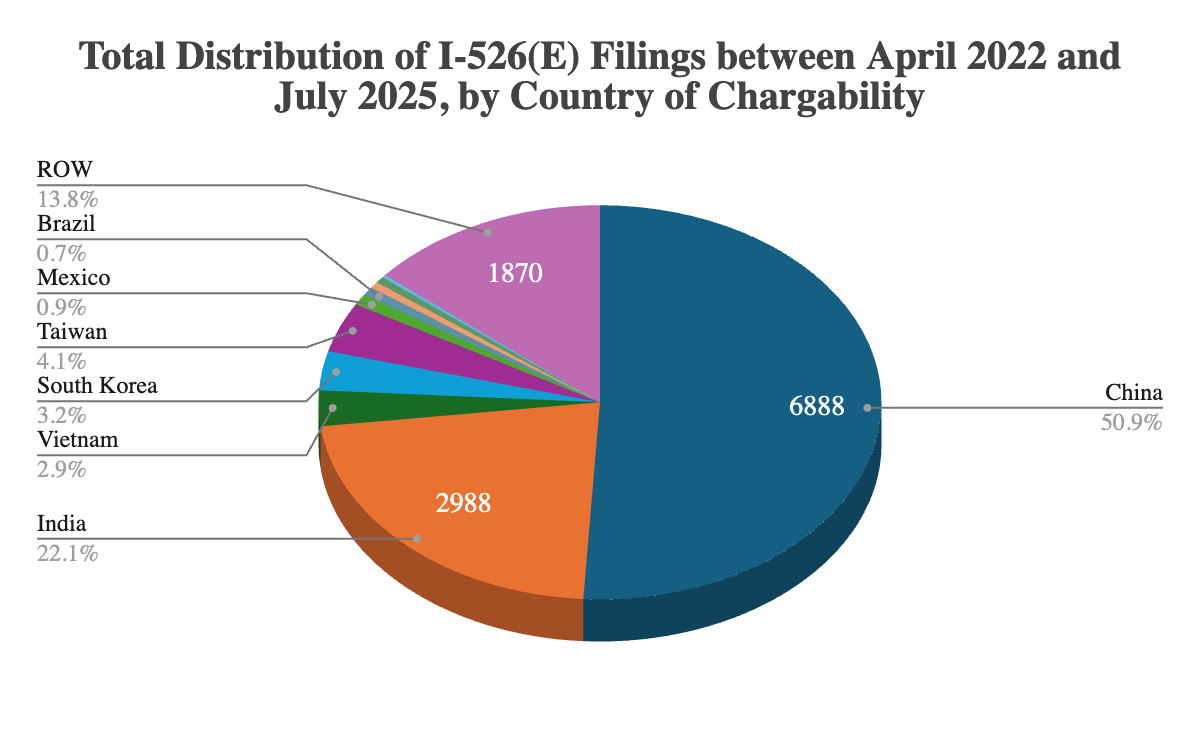

Chuỗi bài viết về Đạo luật Tự do Thông tin (FOIA) của AIIA: Số liệu thống kê cập nhật về hồ sơ I-526E tháng 7 năm 2025

AIIA đã thu thập được dữ liệu mới theo Đạo luật Tự do Thông tin (FOIA) tính đến ngày 31 tháng 7 năm 2025, tiết lộ cách USCIS thực sự xử lý các đơn xin EB-5, cho thấy việc ưu tiên xử lý rất cao...

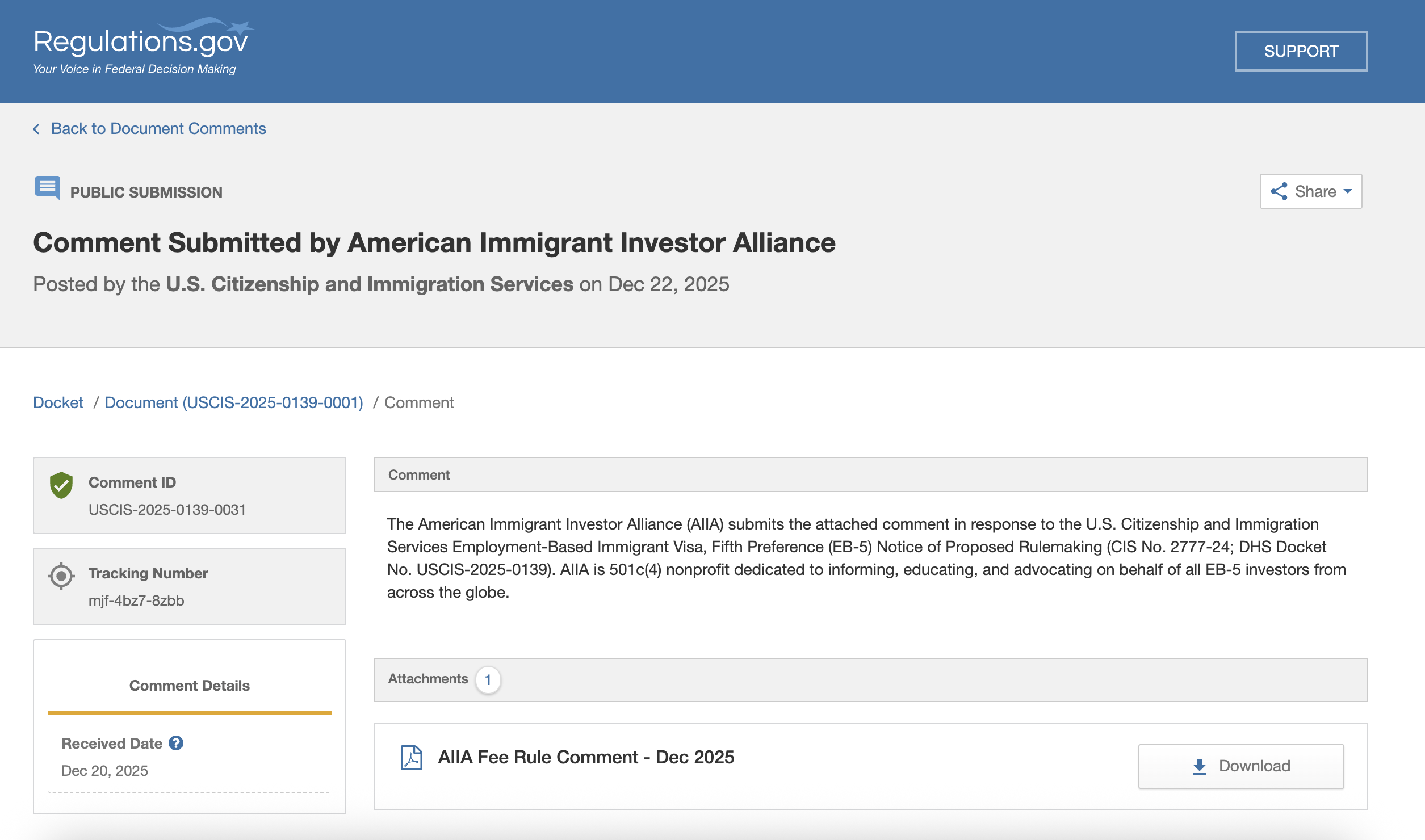

Tìm hiểu thêmHiệp hội Đầu tư Nước ngoài Hoa Kỳ (AIIA) gửi ý kiến đóng góp về Dự thảo Quy định (NPRM) của Sở Di trú và Nhập tịch Hoa Kỳ (USCIS) liên quan đến quy định cập nhật về lệ phí EB-5

AIIA đã gửi ý kiến đóng góp về Dự thảo Quy định về Phí EB-5 tháng 10 năm 2025 của USCIS, trong đó ủng hộ mức phí được điều chỉnh và hợp pháp, nhưng đồng thời kêu gọi hoàn trả số tiền đã nộp thừa...

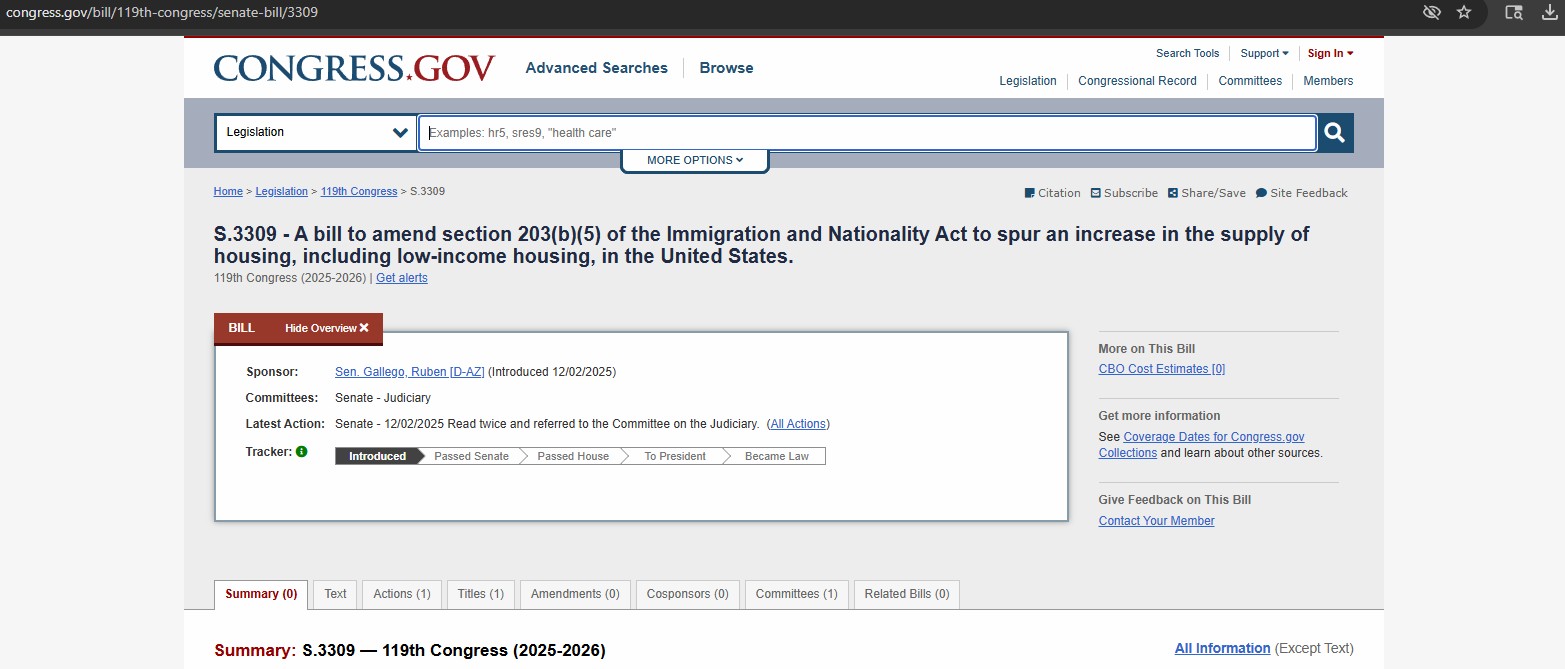

Tìm hiểu thêmChúng tôi xin chúc mừng Thượng nghị sĩ Gallego về dự luật mới tận dụng Chương trình EB-5 để xây dựng nhà ở giá rẻ.

Dự luật EB-5 của Thượng nghị sĩ Gallego huy động vốn nước ngoài để xây dựng nhà ở giá rẻ. Sự hợp tác này đã củng cố mối quan hệ và uy tín của AIIA với Quốc hội...

Tìm hiểu thêmChúng tôi đã thắng kiện vụ kiện về việc tăng phí EB-5.

AIIA đã thắng kiện thành công trong vụ kiện chống lại việc tăng phí EB-5 của USCIS vào tháng 4 năm 2024, với phán quyết của một thẩm phán liên bang rằng cơ quan này...

Tìm hiểu thêmLiên hệ với chúng tôi

Nếu quý vị có bất kỳ câu hỏi, thắc mắc hoặc đề xuất hợp tác nào, xin vui lòng liên hệ với chúng tôi mà không ngần ngại.

Thanks for sharing such a useful info.