AIIA FOIA Series: Source of Funds Review at I-829 stage

18th February, 2023

USCIS has provided some information on the re-adjudication of Source of Funds are I-829 stage, but much of it is redacted. The article also focuses on the issue of re-examining the source of funds and path of funds used by investors. AIIA says that this scrutiny can be unfair to investors who used informal methods to transfer funds.

Background: Last year, AIIA filed a Freedom of Information Act (FOIA) request requesting data from the USCIS on various topics that concern immigrant investors. These included staffing numbers at the Immigrant Investor Program Office (IPO), up-to-date and accurate inventories of pending petitions by country of chargeability, information regarding administrative policies on I-829 processing criteria and implementation of certain provisions of the Reform and Integrity Act of 2022. When we failed to receive this information within the statutory time period, we began litigation against USCIS in order to compel them to comply with our lawful FOIA request. We have recently reached an agreement for monthly document productions in response to our request. We received the first few batches, including hundreds of pages of internal memos, emails and training manuals. If you are an AIIA member and would like to receive the full copy of the government’s FOIA response, reach out to us through our contact form.

In our recent update about AIIA’s visit to Vietnam, we announced that we had filed a Freedom of Information Act (FOIA) request seeking answers to questions that many investors and attorneys have not received any information on, particularly focused on some of its processing pipelines. We have filed additional FOIA requests inquiring about IPO processing times, procedures, approval and denial rates, and staffing statistics.

The Freedom of Information Act (FOIA) is a federal law that requires the full or partial disclosure of previously unreleased or uncirculated information that is controlled or under the possession of the US government or public agencies. FOIA is intended to make US government agencies functions more transparent to the American public. When a member of the public submits a request for government information, the specific agency holding the requested information has broad discretionary powers over what information is disclosed to the public. However, any public authority is subject to the FOIA, including USCIS, the Department of State, and the IPO.

We have witnessed the IPO severely curtailing public engagements and dissemination of information to the public in the past few years. This has led to a huge pent-up demand for EB-5 petition data (processing, inventory, etc) which this FOIA response may help address. AIIA was founded with the objective of making the EB-5 program simply better for investors, we must try and succeed in obtaining information whose knowledge would allow investors to achieve better outcomes. Please consider supporting our work so we can continue to work towards helping the immigrant investor community.

Thanks to the efforts of our legal counsel, USCIS is cooperating to provide all relevant records in relation to the requests we have made. This particular article focuses on the issue of re-examination of lawful source and path of funds during I-829 adjudication.

The specific wording of our request is as follows.

REQUEST: Provide all records which were prepared, created, received, transmitted, collected and/or maintained by the Agency that relate or refer in any way to policies regarding the re-examination of the lawful source and path of EB-5 capital requirement during I-829 adjudication, which is necessarily following a Form 1-526 approval. Please note we seek any such records created on or after January 1, 2017.

Redactions – FOIA responses often have them, but what do they mean?

What we received: The documents we have received so far as part of this response include internal communications and training manuals describing the protocols for reviewing of SOF at the I-829 stage. However, many of the pages were at least partially or completely redacted.

What it means: Three main types of redactions are listed in the documents which we were sent: redaction type (b) (6), (b) (7), and (b) 7(e). b(6) is a FOIA exemption which protects the personal privacy interests of individuals who work at a specific agency. (b)7(e) protects “all law enforcement information that “would disclose techniques and procedures for law enforcement investigations or prosecutions, or would disclose guidelines for law enforcement investigations or prosecutions if such disclosure could reasonably be expected to risk circumvention of the law.” (b)(7) is used to “[protect] from disclosure “records or information compiled for law enforcement purposes””. (b)(7) was the exemption used most often in the disclosed documents to exempt nearly all concrete information pertaining to adjudication of immigrant petitions.

Our take: While these FOIA exemptions, specifically (b) (7) and (b) (7) (e), do permit the USCIS to withhold sensitive information pertaining to their proceedings, as they relate to law enforcement. We, however, believe that basic and concrete information pertaining to sourcing funds and sustainment periods should not have been redacted using this justification, given that these rules universally apply to all investors. We also believe it would be beneficial for immigrant-investors and their attorneys to be aware of the adjudication standards which affect the rate at which immigrant-investor petitions are approved or denied.

The issue of Informal Value Transfers (IVTs)

What we received: Through our FOIA, we received multiple training materials used to train adjudicators at the IPO for the I-829 stage. These are the ‘learning objectives’ for evaluating SOF at the I-829 stage from one such manual.

What it means: While most of the information was redacted, we found important information concerning informal value transfers (IVTs) and currency swaps used by EB-5 investors. IVTs are defined by the USCIS as “any system, mechanism, or network of people that receives money for the purpose of making the funds, or an equivalent value, payable to a third party in another geographic location, whether or not in the same form”. The agency holds interest in regulating IVTs as a matter of “financial intelligence” to prevent money laundering, funding of terrorism, and other financial crimes from being used within the EB-5 immigration program.

Our take: We understand the intent behind the USCIS scrutinizing IVTs more closely given the potential for misuse of inappropriate funds within the EB-5 program. However, it is also the case that IVTs, as informal as they may be in the US, are a common part of commercial transactions and trade in many countries. Many nations have influenced their banking institutions to enforce severe export caps in order to manage their currency supplies which leaves many investors and indeed much of the legitimate foreign trade in these countries to rely on the IVT system. Many investors have utilized IVTs in countries such as China and Vietnam, to fund new commercial enterprises in the US.

Documents suggest that USCIS has a policy of deferring to decisions about IVT made by I-526 adjudicators, when re-evaluating applications at the I-829 stage. However, reality suggests that disproportionate and growing rates of I-829 petition denials in countries such as China and Vietnam may mean this is not the case. Most of the information pertaining to re-adjudicating SOF at the I-829 stage was redacted, therefore we cannot yet know what specific standards the agency holds IVTs to, and what type of RFE responses I-829 adjudicators find acceptable. In a specific instance, text suggesting “officers assigned a form I-829 should ___.” was redacted. What we can conclude from all this is that there may be very limited scope for avoiding re-examination of SOFs at the I-829 stage, for petitioners who have utilized IVTs to fund their new commercial enterprise.

IVTs and Path of Funds Issues

What we received:

What it means: USCIS memos suggest that currency swap issues may also come from failure to include source of funds from the individual or company conducting the currency swap for the petitioner. Therefore, if an individual investor uses an IVT service to invest into the EB-5 program, they would need to include the service’s Source of Funds in the documents submitted with immigration petitions. This can be problematic for investors who utilized services years ago that may not exist anymore or cannot get further documents from.

It appears that deference is given to previously adjudicated SOF other than when there are certain exceptions. Redactions prevent us from knowing what these exceptions are What we can glean from this manual is that deference may not apply when individuals used a third party to exchange funds – whether the third party exchanger is a friend, use of the “hawala” system, and even if the third party exchanger is licensed. Therefore, it is safe to assume that re-adjudication of funds at the I-829 stage is a prescribed requirement that USCIS has to re-scrutinize investors using IVTs and other third-party currency swaps from moving into their conditional residency period.

The presence of an IVT tracker tool goes on to show that the agency takes tracking IVTs quite seriously and there is an effort to map IVTs, presumably with an effort to triangulate IVT service providers who may have serviced many petitioners. References to currency swaps in Chinese Yuan, Vietnamese Dong and Pakistani Rupees can be found. Another reference indicates that affidavits do not generally hold weight when responding to an RFE or in the initial application. This shows that the agency has set the burden of proof quite high (higher than more likely than not) when it comes to IVTs.

![]()

Our take: It is clear that re-adjudications of SOFs at I-829 is a real concern. The (b) (7) (e) redactions go on to show that USCIS considers the subjects of these redactions matter of law enforcement techniques. The implication is that USCIS would prefer to catch petitioners on the wrong side of their internal policies, rather than disclose what those policies are so applicants can avoid being on the wrong side of them altogether. Future investors would be well-advised to be very cautious with IVTs and perhaps avoid them altogether. We have to believe that USCIS developed some of its policies on IVTs well after many of these IVTs were allowed during the I-526 adjudication process. Otherwise, why not apply all this scrutiny during the I-526 stage?

We feel that these redactions should be disclosed, given that these rules dramatically affect the types of immigrant petitions which qualify for approval and re-adjudication, as well as the advice which immigration attorneys may provide to their clients. Keeping these protocols undisclosed not only makes the adjudication process less efficient, but also works against investors by imposing undisclosed requirements on their applications, leading to higher and unpredictable denials.

What comes next?

We are still anticipating additional responses to our multiple FOIA requests. We expect to receive more of these documents in the near future and will release helpful summaries of our findings. IVTs continue to remain a particular area of interest given the number of investors affected by this policy. See our previous blog post to learn about the real impact this is having in affected source countries of this capital.

If you are a member of the EB-5 community and would like to receive further information pertaining to the FOIA response, please reach out to us through our contact form. We will continue to receive incremental updates to our original FOIA requests in the months to come, and will update our AIIA community with further relevant topics as we learn about them. As always, we look forward to hearing from our community and members.

Furthermore, please consider donating to our organization so we can continue our efforts to bring equity and justice in the legal US immigration system and equal access to information for all EB-5 investors across the world. You can support our organization through a donation of any amount here.

Directory of Professionals

AIIA has curated a list of the top professionals from attorneys, investment specialists, to business plan writers to support all EB-5 stakeholders.

View Directory of ProfessionalsRelated Posts

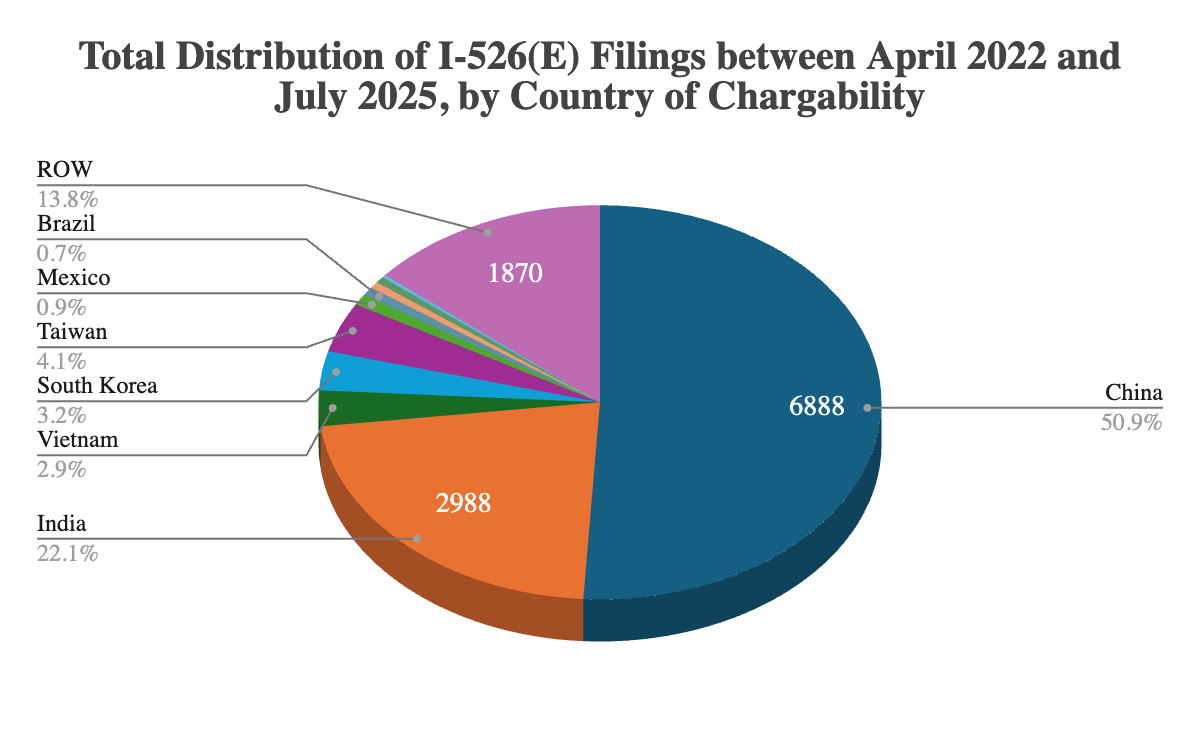

AIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

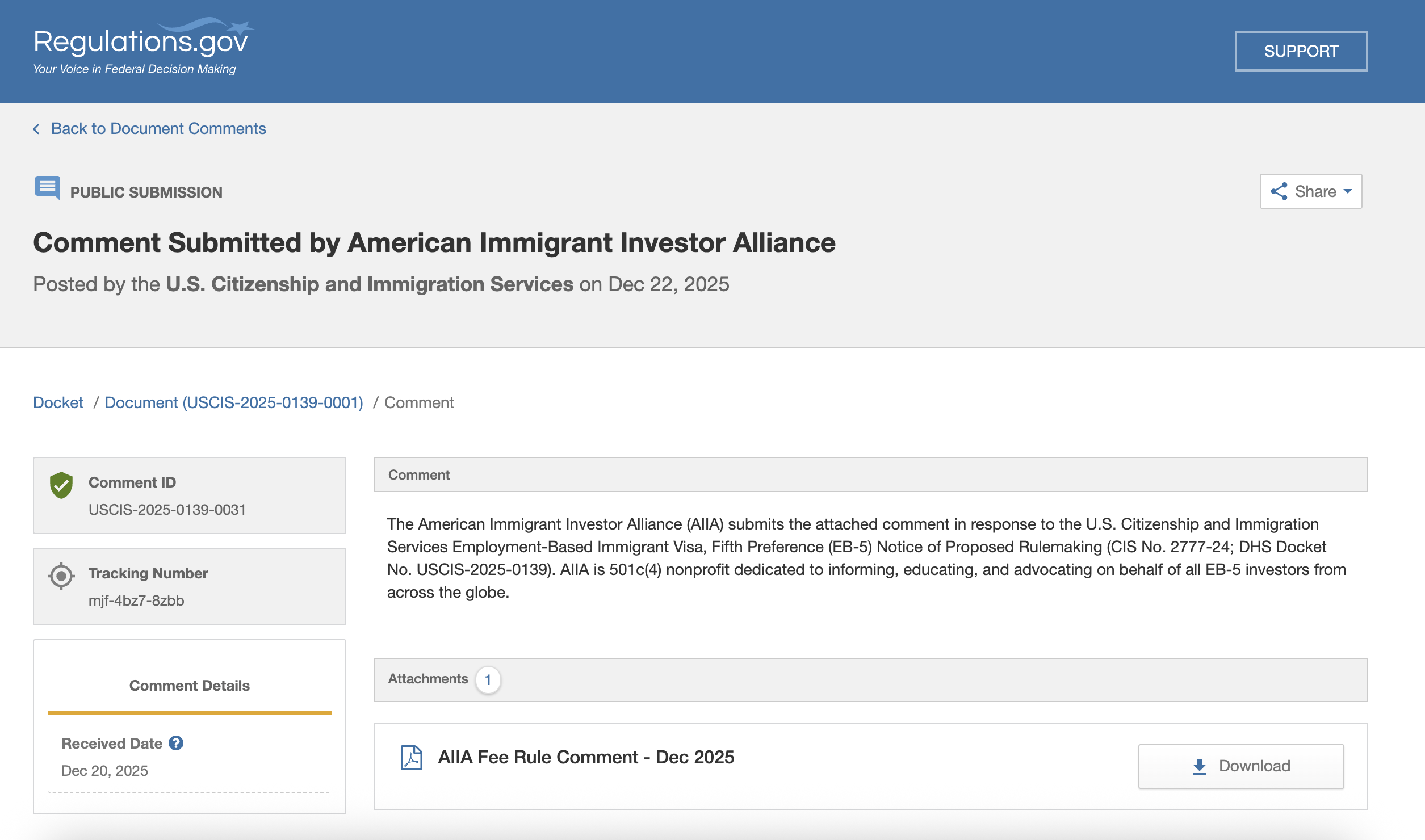

AIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

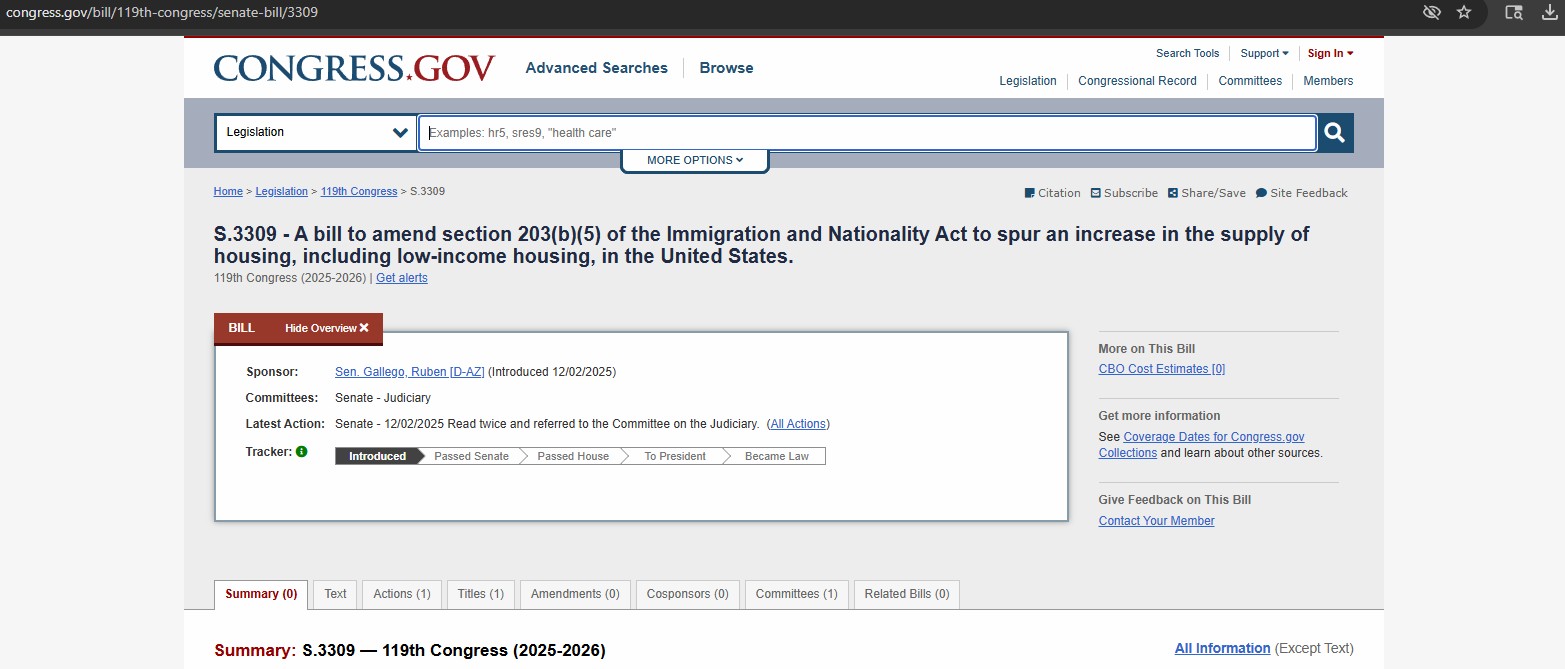

We Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

We Won The EB-5 Fee Increase Lawsuit

Leave your comments

Responses (2)

Directory of Professionals

AIIA has curated a list of the top professionals from attorneys, investment specialists, to business plan writers to support all EB-5 stakeholders.

View Directory of ProfessionalsRelated Posts

AIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

AIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

We Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

We Won The EB-5 Fee Increase Lawsuit

Stay Up To Date With AIIA

Join our newsletter to stay up to date on EB-5 updates.

By subscribing you agree to with our Privacy Policy and provide consent to receive updates from our company.

Recommended Resources

How to find a good EB-5 Litigation Attorney

Choose an attorney with EB-5 and litigation experience who is organized, detail-oriented, and avoids making guarantees. You may need a...

Read More

The Sale of EB-5 Securities Offerings

EB-5 securities sales often use Regulation D (U.S. investors) and Regulation S (foreign investors) exemptions to avoid SEC registration while...

Read More

Choosing between Direct vs Regional Center EB-5 financing

Direct EB-5 suits single investors creating direct jobs; Regional Center EB-5 pools multiple investors, counting direct and indirect jobs for...

Read MoreRecent Blog Posts

AIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

AIIA obtained new FOIA data through July 31, 2025 revealing how USCIS is actually processing EB-5 petitions, showing heavy prioritization...

Learn MoreAIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

AIIA submitted comments on USCIS’s October 2025 EB-5 fee NPRM supporting revised, lawful fee levels but urging refunds for overpaid...

Learn MoreWe Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

Sen. Gallego's EB-5 bill mobilizes foreign capital to build affordable housing. This collaboration has boosted AIIA's Congressional ties & credibility...

Learn MoreWe Won The EB-5 Fee Increase Lawsuit

AIIA successfully won its lawsuit against USCIS’s April 2024 EB-5 fee increases, with a federal judge ruling that the agency...

Learn MoreGet In Touch With Us

If you have any questions, inquiries, or collaboration proposals, please don’t hesitate to reach out to us.

Thas very well good

Can you share me the legal document which mentions how long EB5 investors need to maintain their investment at risk after arriving to the US.?

And after arriving to the US, do EB5 investors need to keep their money at regional center or can put it in any specific funds?