Foreign Investor Fairness Protection Act FAQ and Update

18th November, 2021

An in depth look into AIIA’s updated proposed Foreign Investor Fairness Protection Act designed to protect existing EB-5 investors from program lapses, which has the potential standalone action if necessary.

On July 14, two weeks after the reauthorization of the EB-5 Regional Center program failed, AIIA released the Foreign Investor Fairness Protection Act (FIFPA), a simple, two-page bill designed to ensure that existing EB-5 petitions be “grandfathered” into the EB-5 visa pool, despite the lapse of the Regional Center program. For the last several months, we have been actively promoting FIFPA in Congress and circulating the bill to other stakeholders and legal advisors. Based on feedback we’ve received, and in consultation with our congressional lobbyist, Bruce Morrison, AIIA has updated the language of FIFPA, strengthening it to better protect investor interests.

We’ve compiled a list of frequently asked questions, and their answers, to provide more context for the updates, the importance of the bill, how it protects investors, and the various pathways for it to be passed and put into law. The full text of the bill is provided below.

FAQ Regarding FIFPA

1. What is FIFPA?

The Foreign Investor Fairness Protection Act (FIFPA) is a proposed standalone (meaning single issue) bill that secures the right of existing EB-5 investors to complete the full visa approval process. This means that any investor who filed an I-526 petition with USCIS at any point during which the Regional Center program was authorized will be able to complete the full immigration process. This is often referred to as “grandfathering” pending petitions into the process, even though the Regional Center Program is no longer authorized.

2. Who Does it Protect?

Anyone who filed an I-526 petition with USCIS before June 30, 2021. This also includes investors that are already further along in the immigration process, including those with pending I-485 or DS-260 applications, or with conditional green cards.

3. What Updates Have You Made?

The revised version of FIFPA expressly states in the case of a program lapse or termination, visa numbers will remain available to investors who are already in the EB-5 process. Additionally, the revised version ensures that there is no retroactive application of future statutes, regulations, and policies on existing investors.

4. Why Should EB-5 Regional Center Investors Care so Much about FIFPA?

The current lapse of the Regional Center Program has laid bare how vulnerable existing investors are to the volatility and politics surrounding the EB-5 Regional Center and its reauthorization. Regardless of the status of the program (now and in the future), investors must have protections in place to ensure that they can see their pathway to immigration through to the end. Without proper grandfathering legislation, the devastating impact of the program lapse on investors and their families today will only be repeated for future investors every time the program lapses.

One of AIIA’s core tenets is that the immigration and investment framework to which investors committed to must remain viable so they retain the opportunity to complete their immigration journey. This principle is critical to the foundation of the EB-5 program, as it instills confidence in current and future investors alike that USCIS gives credence to the experience of prospective EB-5 immigrants.

5. Why Does Grandfathering Need to Be Achieved Through A Piece of Legislation and Not Enforced Through Existing Laws?

The original law provided that the EB-5 Regional Center “Pilot” Program (as it was originally called) would be temporary and subject to continued extension by the United States Congress. Upon the statutory expiration of the program, USCIS will not accept new I-526 filings (or new I-924 applications for regional centers) for petitions filed with a regional center project. USCIS’s current policy also stipulates that, upon the expiration of the program, processing will be paused for any pending I-526 petitions and pending green card applications which may be based upon an approved I-526 petition.

The U.S. Department of State adheres to the same policy and places a hold on any DS-260 applications or the scheduling of interviews for EB-5 Immigrant Visa issuances. Some U.S. federal courts have also interpreted the sunset and expiration of the Regional Center Program as removing USCIS’s authorization to continue to process any pending I-526 petitions. Because there is no avenue for investors to pursue in the current legislative framework, grandfathering can only be achieved through new legislation.

6. Can FIFPA Be Pushed as A Standalone Measure?

Yes it can, and we will keep this as an option for the path forward. But our immediate priority is getting FIFPA written into law as soon as possible, and the current EB-5 Regional Center reform bill that is circulating in Congress is the best path forward today.

We recognize that any further delay in the processing of investors’ petitions will be extremely painful for every member of AIIA and all investors. However, we believe that it would be counterproductive at this stage to push FIFPA as a standalone piece of legislation, independent of the Regional Center reform bill. We will continue to circulate and promote FIFPA among members of Congress to build support for grandfathering, but there is no appetite in Congress right now for piecemeal EB-5 legislation. Because Congress needs to see the EB-5 industry as aligned and cooperating, not divided into different interest groups, AIIA is willing to work side-by-side with members of the industry to arrive at a final bill that will adequately protect existing investors while also achieving long-term reauthorization and long-needed reform to the Program.

7. What if the Regional Center Reform Bill Fails to Pass by the End of the Year?

As we outlined in our last newsletter, we do expect this to be the case, primarily because it is unlikely that Congress will agree upon and successfully pass the legislative vehicle that the EB-5 reform bill will be attached to. The EB-5 industry disagrees with our assessment and believes that the reform bill will be enacted into law by the end of the year. Despite our differing views, we fully support the industry and its push for a reform bill.

In the event the reform bill fails to be passed by the end of 2021, we may push FIFPA as a standalone measure to be hotlined in the Senate. This is a process by which legislation can bypass typical Senate procedures and be brought to a vote with little or no floor debate but must be passed by unanimous consent. By December, investors will have waited nearly six months for their petitions to resume processing and for their green cards to be issued. [Lack] of successful reform legislation at the end of the year, we believe hotlining will be the most effective, and fastest, avenue to give investors reprieve. If FIFPA is passed through this process, we will continue to provide support and assistance to the EB-5 industry to ensure the broader reform bill is passed next year.

AIIA-Foreign Investor Fairness Protection Act-revised-10-22-21.pdf

Directory of Professionals

AIIA has curated a list of the top professionals from attorneys, investment specialists, to business plan writers to support all EB-5 stakeholders.

View Directory of ProfessionalsRelated Posts

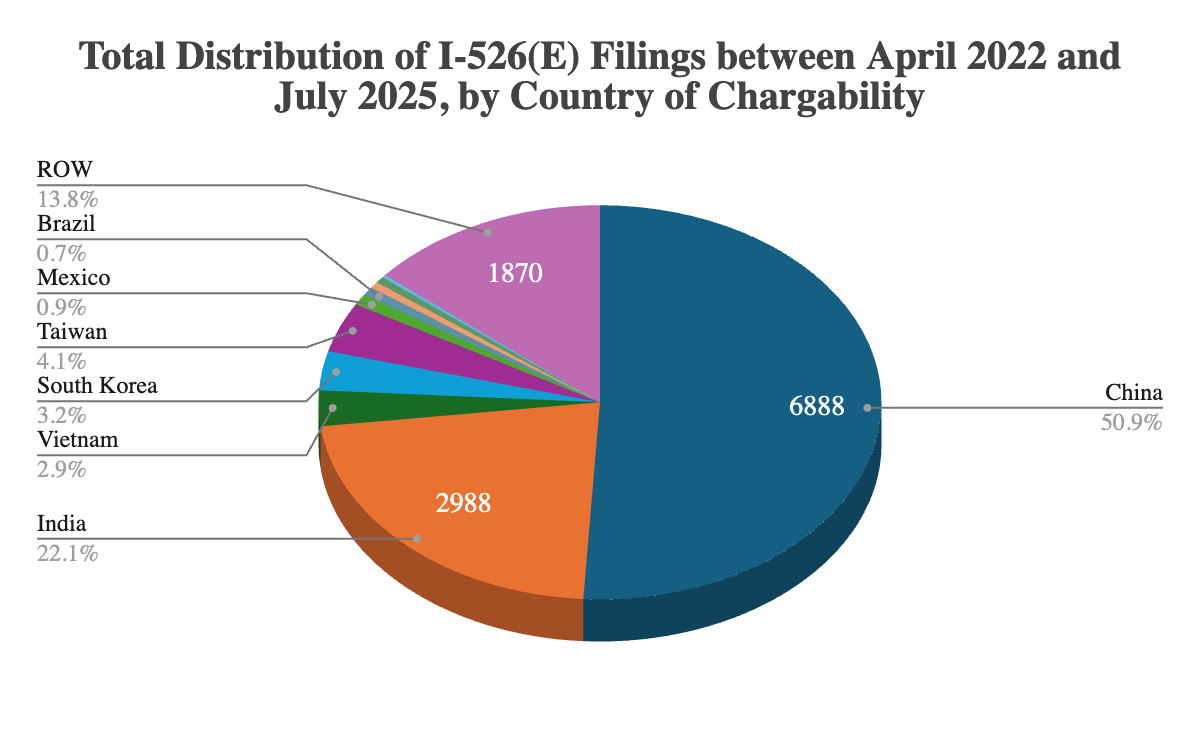

AIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

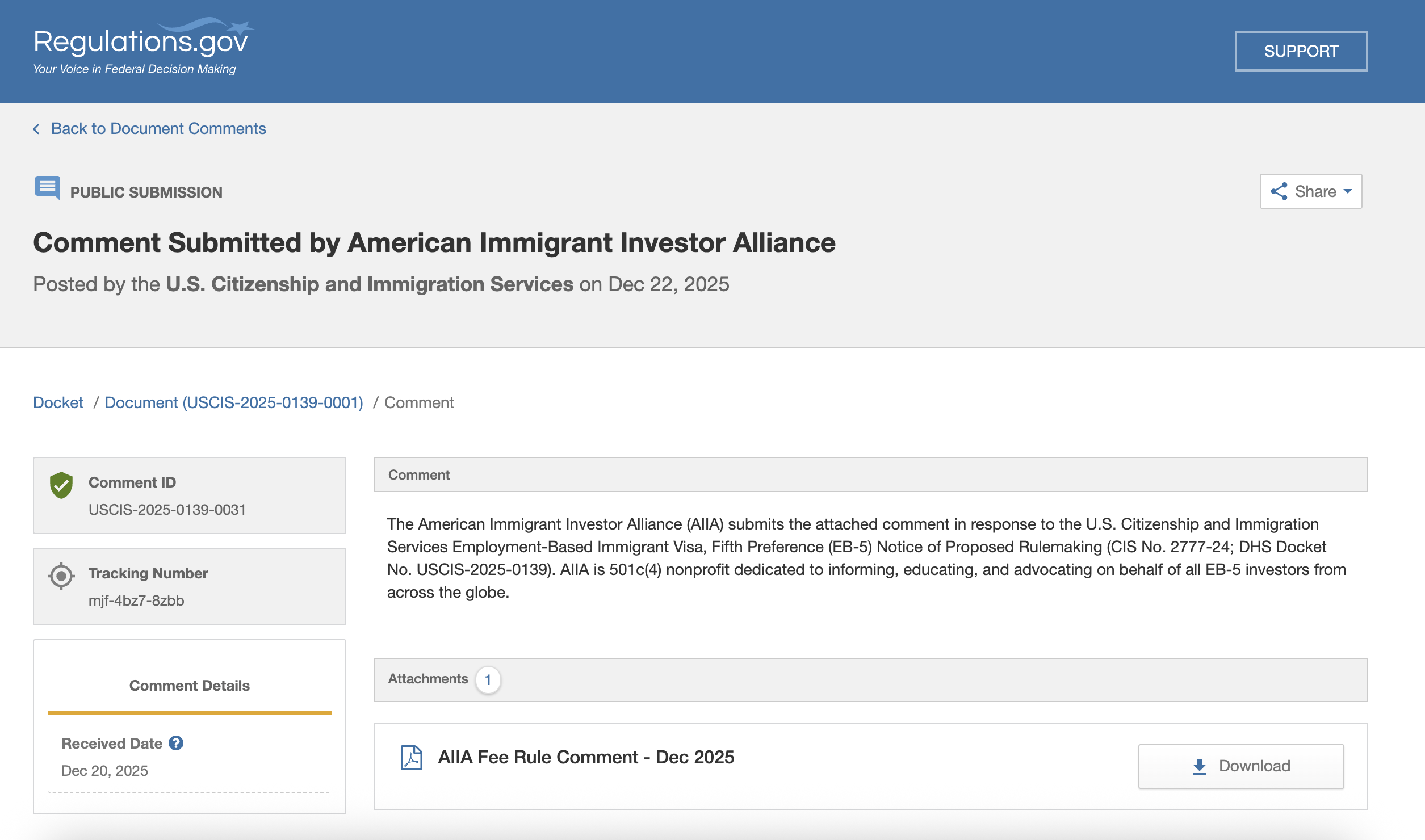

AIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

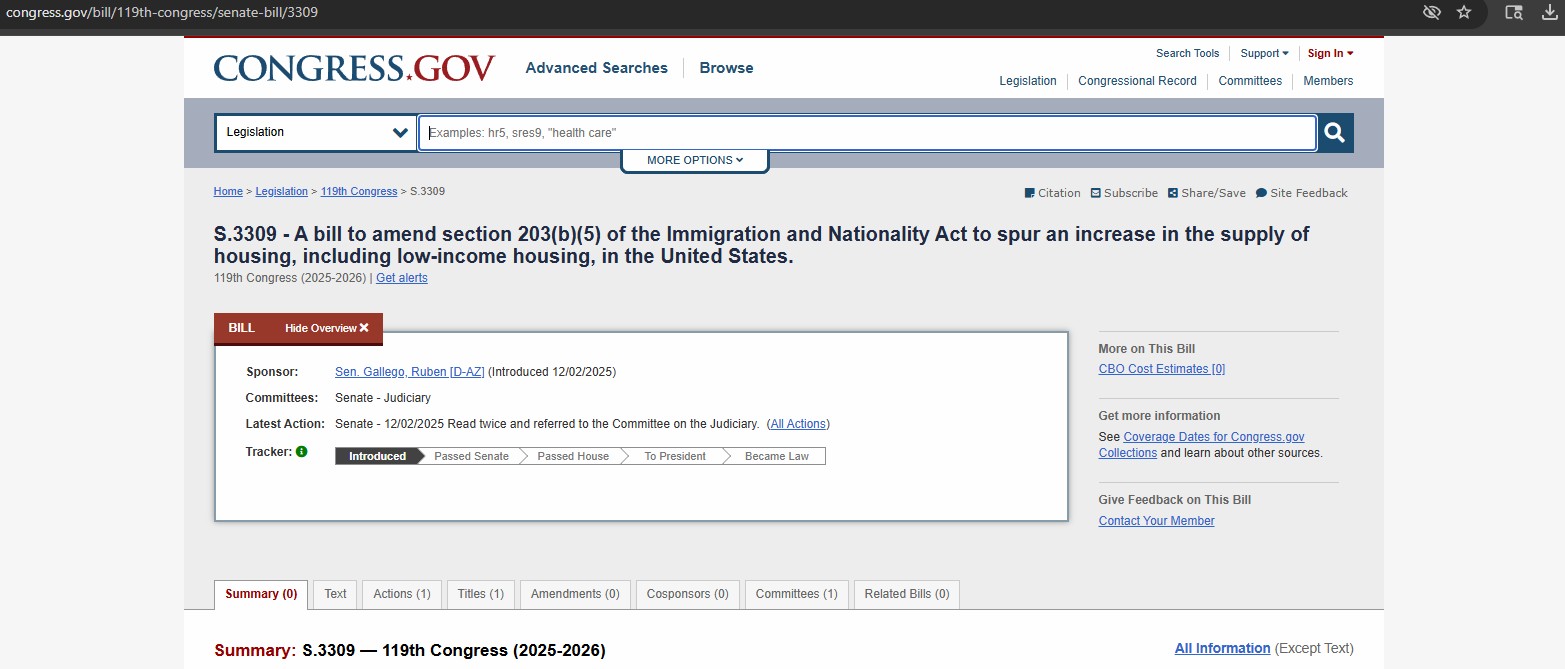

We Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

We Won The EB-5 Fee Increase Lawsuit

Directory of Professionals

AIIA has curated a list of the top professionals from attorneys, investment specialists, to business plan writers to support all EB-5 stakeholders.

View Directory of ProfessionalsRelated Posts

AIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

AIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

We Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

We Won The EB-5 Fee Increase Lawsuit

Stay Up To Date With AIIA

Join our newsletter to stay up to date on EB-5 updates.

By subscribing you agree to with our Privacy Policy and provide consent to receive updates from our company.

Recommended Resources

The Issue of Aging Out in EB-5

The Child Status Protection Act (CSPA) helps freeze a child’s age on EB-5 petitions, but long visa backlogs still risk...

Read More

The Sale of EB-5 Securities Offerings

EB-5 securities sales often use Regulation D (U.S. investors) and Regulation S (foreign investors) exemptions to avoid SEC registration while...

Read More

Choosing between Direct vs Regional Center EB-5 financing

Direct EB-5 suits single investors creating direct jobs; Regional Center EB-5 pools multiple investors, counting direct and indirect jobs for...

Read MoreRecent Blog Posts

Class Action Lawsuit Filed Against USCIS for EB-5 Fee Refunds

Did you pay inflated EB-5 filing fees after April 2024? AIIA has filed a federal class action lawsuit against USCIS...

Learn MoreAIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

AIIA obtained new FOIA data through July 31, 2025 revealing how USCIS is actually processing EB-5 petitions, showing heavy prioritization...

Learn MoreAIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

AIIA submitted comments on USCIS’s October 2025 EB-5 fee NPRM supporting revised, lawful fee levels but urging refunds for overpaid...

Learn MoreWe Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

Sen. Gallego's EB-5 bill mobilizes foreign capital to build affordable housing. This collaboration has boosted AIIA's Congressional ties & credibility...

Learn MoreGet In Touch With Us

If you have any questions, inquiries, or collaboration proposals, please don’t hesitate to reach out to us.

Responses (0)