How to Financially Prepare for An EB-5 Investment while Working on the H-1B

30th January, 2024

In this guide co-written by Vrishin from CapitalWe and AIIA, we explored the different methods which prospective EB-5 investors on H1-B visa can best prepare for their eventual investment.

For many young immigrant professionals in the United States, the H-1B visa system presents a myriad of challenges and uncertainties. As a financial planner specializing in this group, I frequently witness their anxieties and frustrations stemming from the unpredictability of their immigration and employment status. If they want to change jobs or lose their jobs unexpectedly, they have to find another employer who can sponsor them and file a new H-1B petition, which can be costly and time-consuming. Sometimes, they may have to stay in low-paying or abusive workplaces just to keep their visa status. They also have to deal with the lottery system, the cap on visas, the frequent policy changes, and the potential fraud and abuse by some employers and intermediaries. Moreover, they may not be able to bring their family members who are not eligible for an H-4 visa, such as adult children and elderly parents, which can result in family separation and emotional distress.

For the average H-1B holder, one petition filing can secure green cards for the investor, their spouse, and any children born outside the U.S. Preparation for filing includes securing $800,000 for the investment, an additional $50,000-$80,000 in administrative and professional service costs, and ensuring all funds are well-documented by official sources. An EB-5 project typically doesn’t repay investors until after six to seven years and that too is an “at risk” investment. For this reason, I always recommend that immigrant investors maintain a financial safety net before making this investment.

For H-1B holders seeking permanent residence in the U.S, the EB-5 visa places no conditions on applying, making it ideal for those who wish to avoid backlogs in the EB-1 and EB-2 categories. Petitioners need not know English, hold any type of special honors, degrees, work sponsorships, or have any outstanding abilities to apply. The only conditions required are a whole, sustained investment in a commercial enterprise, ten jobs which are generated through your investment, and a legal source of funds for the investor and their family.

In this blog below I detail some of the common methods my clients and other H1B holders typically finance their investments and what you can do now to start preparing for this investment.

To navigate these financial demands, H-1B holders typically utilize the following options to fund their EB-5 Investment

- Savings: High-earning professionals living in low-cost areas can accumulate substantial savings through diligent budgeting and disciplined spending habits.

- Retirement Accounts: Individuals with sizable 401(k) balances may be able to borrow against these funds through a 401(k) loan, avoiding early withdrawal penalties and preserving retirement savings.

- Home Equity: Homeowners with significant equity can potentially secure a home equity line of credit (HELOC) to finance their EB-5 investment.

- Taxable Brokerage Accounts: Investors with substantial holdings in stocks or bonds can consider a securities-backed line of credit (SB-LOC) to leverage their assets.

- Funds from Home Country: Sale of property or other assets in the investor’s home country can provide the necessary capital as long as there is formal source documentation available.

- Gifts from Family and Friends: Documented gifts from family or friends can contribute to the investment funds.

- Loans: USCIS permits EB-5 investments funded through loans, provided the investor assumes sole responsibility for the debt and secures it with personal assets rather than those of the investment enterprise. (Unsecured loans are an option as well but it can be very tricky to get large unsecured loans.)

Preparing for the Future: A Proactive Approach

To effectively prepare for an EB-5 investment, H-1B holders should adopt a proactive approach:

Start with getting clear on your goals: Defining what is important to you will help provide clarity on what you need to do with your money. E.g. If staying in the country in the long term is more important than owning a home (in the short term) then you need to save into different accounts than buying real estate.

One clear step: Sit down with a piece of paper and write down what all you want to achieve in 1, 3 and 5 years from now. Reorder these from most important to least important.

Automate savings + Conscious spending: I hate the word “budget” since it has a negative connotation, so I instead recommend that people pay more attention to their spending. You need to automate money movement such that each paycheck you send money into a savings/investment account and spend the rest in a manner that aligns with your values.

One clear step: Start before you are ready. Set up a recurring, automated transfer of $100 from your checking account to your savings/investment account each paycheck cycle (biweekly or monthly). You can then adjust this amount as needed.

Spend more money (on self-development): This may seem counterintuitive, but you need to spend more on education and skill development. We as immigrants don’t do this enough and it is holding back your ability to exponentially increase income (especially lack of soft skills).

You are in a different country and the rules are different, so you need to adapt accordingly.

One clear step: Review your most recent performance review, or set up some time with your manager to ask them what you can be doing better or what soft skills would make you invaluable for the team.

Think long-term + Invest wisely: Realize that it is not a sprint but a marathon. You are going to have a much better result by not trying to get a better-than-average return percentage, but saving a better than average savings percentage.

One clear step: Read any or all of the following books:

“The Little Book of Common Sense Investing” by Jack Bogle

“The Psychology of Money” by Morgan Housel

“The Millionaire Next Door” by Thomas J. Stanley

Read up about the Bogleheads portfolio.

Working with a professional: A CPA is good to have, but I also recommend working with a financial planner who is able to guide your finances keeping in mind your visa challenges and goals.

One clear step: Reach out for a free consultation! I work with immigrants on an H1b who don’t want their job and finances to control their life and immigration. I can help you plan for big purchases like the EB-5. Here is a link to book time.

The EB-5 visa is a very common method for H-1B holders to start their transition into permanent residency in the United States. However, transitioning into this visa requires careful financial preparation and due diligence. To learn more about the EB-5 visa, how the program works, and to learn more about what you need to get started, visit the American Immigrant Investor Alliance’s resource library for prospective EB-5 investors.

Directory of Professionals

AIIA has curated a list of the top professionals from attorneys, investment specialists, to business plan writers to support all EB-5 stakeholders.

View Directory of ProfessionalsRelated Posts

Class Action Lawsuit Filed Against USCIS for EB-5 Fee Refunds

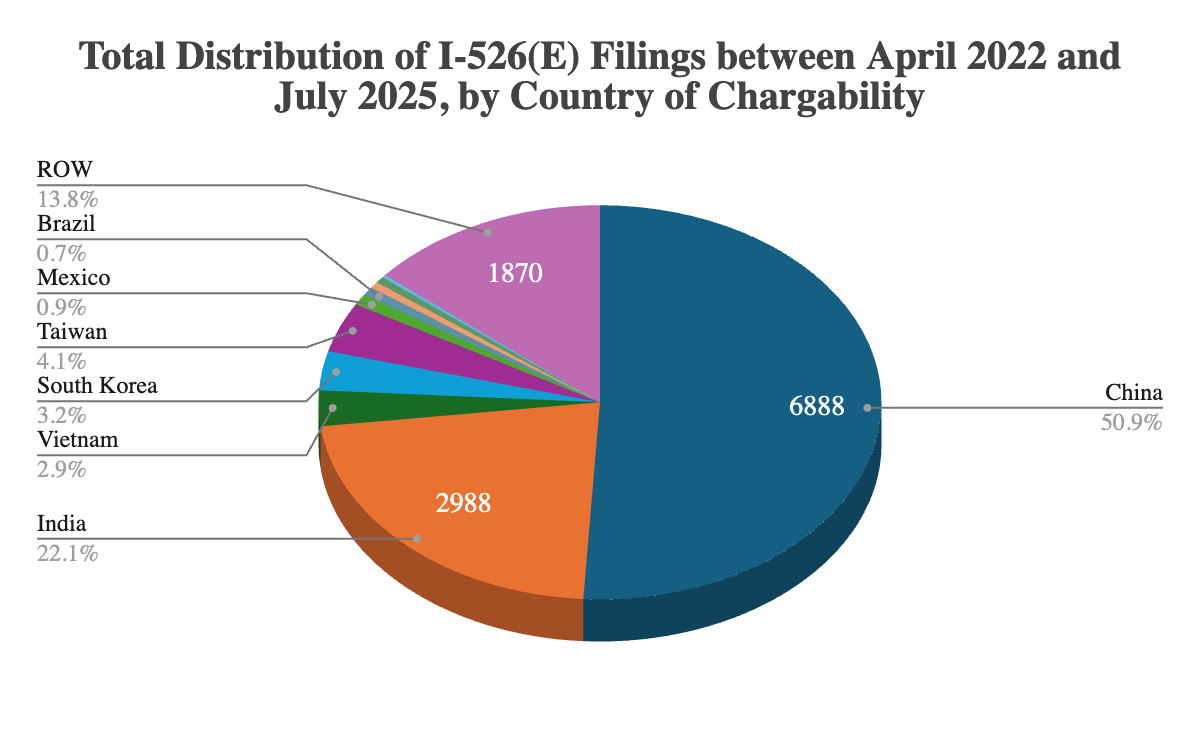

AIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

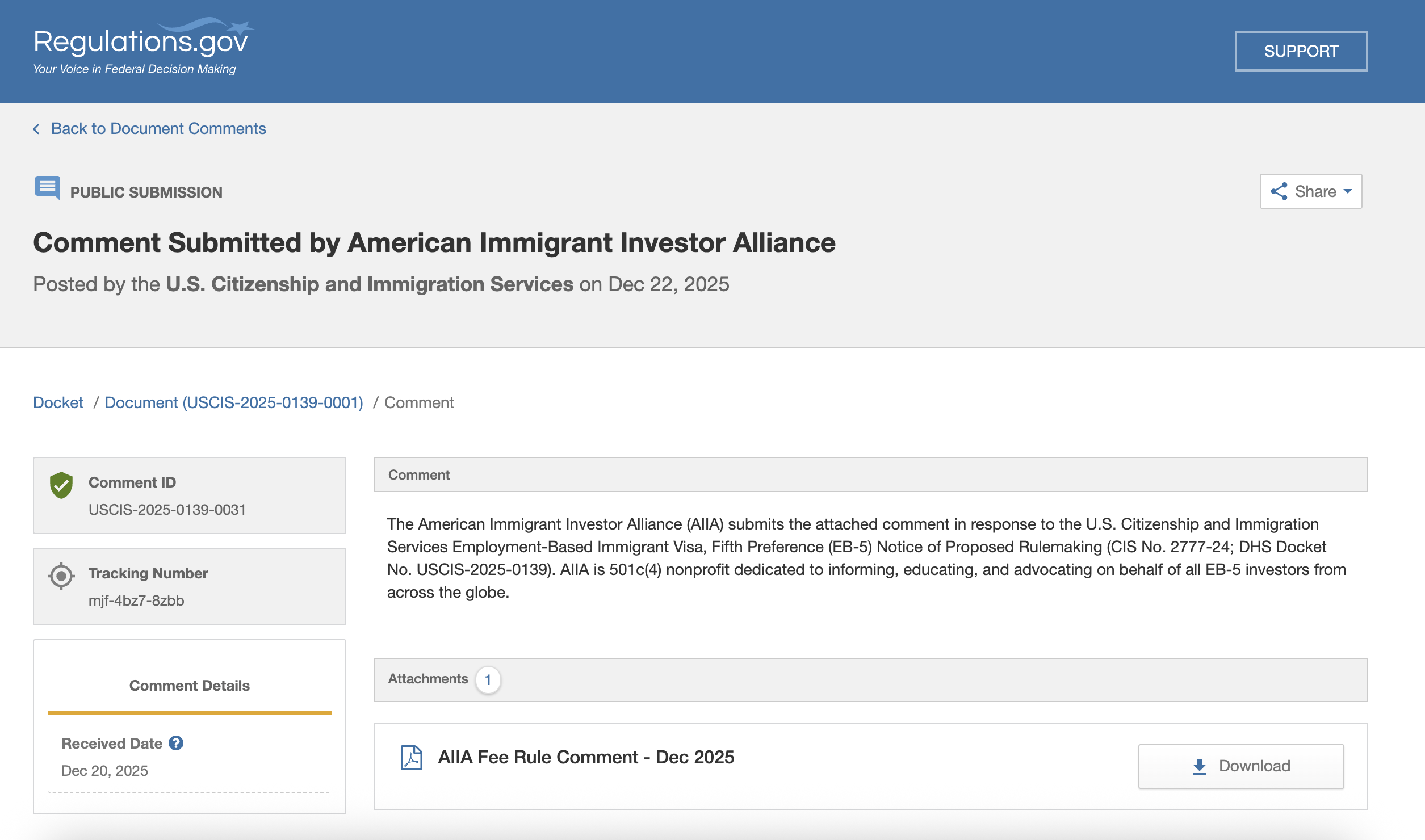

AIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

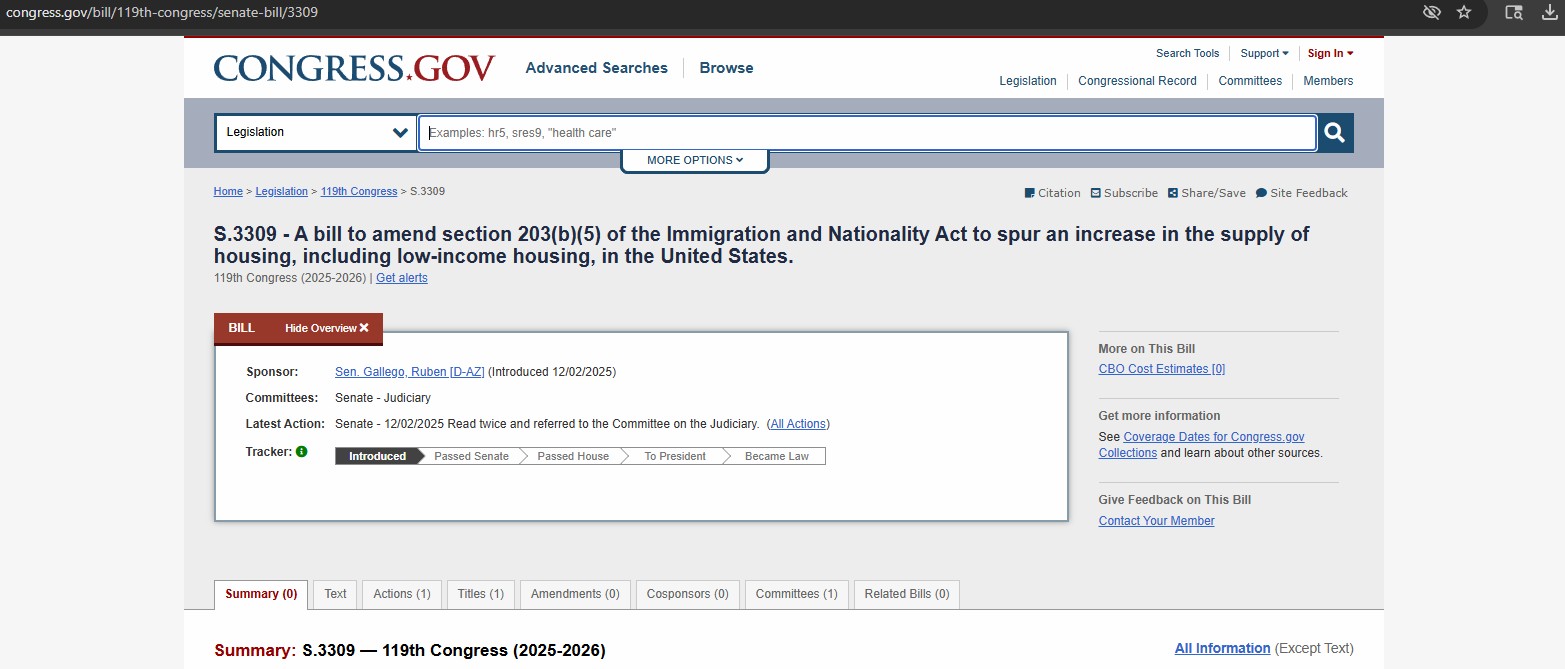

We Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

Leave your comments

Responses (1)

Directory of Professionals

AIIA has curated a list of the top professionals from attorneys, investment specialists, to business plan writers to support all EB-5 stakeholders.

View Directory of ProfessionalsRelated Posts

Class Action Lawsuit Filed Against USCIS for EB-5 Fee Refunds

AIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

AIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

We Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

Stay Up To Date With AIIA

Join our newsletter to stay up to date on EB-5 updates.

By subscribing you agree to with our Privacy Policy and provide consent to receive updates from our company.

Recommended Resources

How to find a good EB-5 Litigation Attorney

Choose an attorney with EB-5 and litigation experience who is organized, detail-oriented, and avoids making guarantees. You may need a...

Read More

The Redeployment Conundrum

Redeployment litigation arises when NCE managers reinvest EB-5 funds without proper judgment, exposing investors to unnecessary risk despite broad contractual...

Read More

“Privity” in EB-5 Litigation

EB-5 issuers often design complex structures and narrow “privity” relationships to make litigation difficult, forcing investors into uphill battles and...

Read MoreRecent Blog Posts

Class Action Lawsuit Filed Against USCIS for EB-5 Fee Refunds

Did you pay inflated EB-5 filing fees after April 2024? AIIA has filed a federal class action lawsuit against USCIS...

Learn MoreAIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

AIIA obtained new FOIA data through July 31, 2025 revealing how USCIS is actually processing EB-5 petitions, showing heavy prioritization...

Learn MoreAIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

AIIA submitted comments on USCIS’s October 2025 EB-5 fee NPRM supporting revised, lawful fee levels but urging refunds for overpaid...

Learn MoreWe Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

Sen. Gallego's EB-5 bill mobilizes foreign capital to build affordable housing. This collaboration has boosted AIIA's Congressional ties & credibility...

Learn MoreGet In Touch With Us

If you have any questions, inquiries, or collaboration proposals, please don’t hesitate to reach out to us.

Thanks for sharing such a useful info.