IIUSA fails to come to an agreement with USCIS on sustainment period

16th March, 2025

AIIA is opposing an IIUSA lawsuit that could lengthen the EB-5 sustainment period for post-RIA investors, undermining the 2-year rule set by Congress. A recent hearing went poorly for our side, and while current rules remain in effect for now, a settlement or court ruling could revert to harmful pre-RIA timelines, so AIIA is preparing legal and advocacy actions to protect all investors.

For several months, the American Immigrant Investor Alliance (AIIA) has been monitoring a civil legal action that could negatively affect post-RIA EB-5 investors. The case, Invest in the U.S.A. (IIUSA) v. U.S. Department of Homeland Security , is currently underway in the U.S. District Court for the District of Columbia. IIUSA seeks to force DHS — specifically, its constituent agency, U.S. Citizenship and Immigration Services (USCIS) — to change the “sustainment period” for post-RIA EB-5 investments (i.e., the amount of time that funds must remain invested to qualify for Lawful Permanent Resident or ‘LPR’ status). Currently, the post-RIA sustainment period is a minimum of two years following the first date of the funds being invested. The regional centers leading IIUSA seek to force USCIS follow formal notice and comment rulemaking to change the duration. Until a new rule is published, the sustainment period could revert to a much longer duration, such as the 2-year post-conditional residence period used for pre-RIA investors.

AIIA has vigorously opposed IIUSA’s action, which is plainly contrary to the text of the EB-5 Reform and Integrity Act (RIA) of 2022. The RIA changed the sustainment period — from two years following the grant of conditional LPR status, to its present period of two years following the first date of the funds being invested. This change is textual and unambiguous in RIA. See Immigration and Nationality Act (INA) § 203(b)(5)(A)(i) (codified at 8 U.S.C. § 1153(b)(5)(A)(i)) (“…which is expected to remain invested for not less than 2 years;…”).

IIUSA seeks to undermine this plain critical reform of the RIA and prevent investors to withdraw their capital in a timely manner without being held at the mercy of the monthly visa bulletin’s final action dates (i.e., visa backlogs) based on their country of birth (e.g., India-born and Mainland China-born petitioners). The new sustainment period ensures fair treatment of EB-5 investors and prevents investor exploitation. The previous status quo benefited EB-5 regional centers (whom IIUSA represents), as they could redeploy the capital of pre-RIA investors affected by visa backlogs for many years, with little oversight and control by investors over the use of their funds. The pre-RIA structure satisfied the self-interest of the investment issuers, and was terrible for EB-5 investors — many of whom invested their life savings in the process, only to be denied the return of their funds for years on end.

In the current challenge to the new, fair post-RIA sustainment period, AIIA filed an amicus brief — i.e., a “friend of the court” brief, which allows non-parties to make legal arguments in a case — supporting USCIS’s position that the 2-year sustainment period was the natural reading of the RIA. Our brief presented the views of immigrant investors on this subject, including the exploitation of investors under the prior regime.

The January 28 hearing, as we have previously discussed, was adverse for our position. The presiding judge, unfortunately, appeared inclined to rule in favor of IIUSA’s position that a formal rulemaking was required to institute a new sustainment period. Anticipating an adverse ruling, we here provide a detailed description of that hearing, news of the most recent developments in the case, and our plans to respond in defense of EB-5 immigrant investors.

The Hearing: DHS fails to persuade the judge

We previously summarized the hearing on January 28, 2025, in our blog post on January 31. To reiterate, the presiding judge — The Honorable Ana Cecilia Reyes, a United States District Judge appointed by President Joseph R. “Joe” Biden, Jr. — signaled that she would likely rule in favor of IIUSA in the case.

Our analysis of the oral argument’s transcript yields the following reasons for this conclusion:

- Total Investment: Judge Reyes questioned whether the new, post-RIA sustainment period (of two years from the date of investment) would increase or decrease total investment in the United States. The attorney for the DOJ, Ms. Faso, missed an opportunity to explain that the total quantum of investment available to RCs is immaterial.

- Fraud and Abuse: Judge Reyes asked for reasons why a shorter sustainment period, created by the RIA, would reduce fraud and abuse. Ms. Faso could not convince the judge that the exploitation of investors by RCs’ redeployment of investor capital is highly abusive and unfair.

- Rulemaking: Judge Reyes questioned whether DHS, specifically USCIS, could determine of its own accord that the RIA created a two year sustainment period from the first date of the investment. The judge disagreed with the the arguments advanced in the briefs: (1) that the statute’s plain language is unambiguous; (2) that the departure from previous language in the RIA indicates Congress’s intent to abandon the previous sustainment period linked to conditional LPR status; and (3) that IIUSA is seeking, in bad faith, to effectively amend the RIA because Congress disadvantaged them.

- DHS Contradictions: Ms. Faso indicated that USCIS had undertaken notice-and-comment rulemaking for previous regulations regarding the EB-5 program. She also indicated that USCIS was, at present, engaged in preliminary stages of such rulemaking regarding the program’s compliance with the RIA. She did not distinguish between those efforts and USCIS’s interpretation of the plain language of the RIA regarding the sustainment period. At this point, Judge Reyes asked Ms. Faso whether USCIS would also be using the notice-and-comment rulemaking process to regulate the sustainment period. Ms. Faso did not have USCIS’s answer.

In sum, Judge Reyes indicated that she would rule as follows:

The RIA’s sustainment period was not plain and unambiguous, and thus the notice on the USCIS website regarding this interpretation was unlawfully promulgated (i.e., it was a “final rule,” which cannot be issued without notice-and-comment rulemaking).

Judge Reyes’s exact quote from the court transcript (p. 41) is as follows:

“If I have to decide this opinion, I don’t know exactly what it’s going to say, but it’s not going to say that the memo was not final, and it’s not going to say that you didn’t violate the APA. So it’s going to say – however it comes out, it’s going to come out for those guys, for the other guys [i.e., IIUSA] and not you [i.e., DHS and AIIA].”

The Joint Status Report

At the conclusion of the hearing, Judge Reyes asked the parties, IIUSA and DHS, to confer with each other and submit a “joint status report” (JSR) to the Court regarding their conference. Given that Judge Reyes indicated her intention to rule in IIUSA’s favor, as well as the protracted nature of an appeals process (to the U.S. Court of Appeals for the District of Columbia Circuit), she indicated that a conference process could help the parties reach a settlement that would end the case without further action. The JSR was due to be submitted within 30 days following the hearing, i.e., by or on February 28, 2025.

On February 27, 2025, the parties filed the JSR with the Court. A copy of the JSR can be found here. Our summary of the JSR is exhibited below.

Following the conference, IIUSA and DHS/USCIS remain in disagreement on how to proceed with the case. Temporarily, this is good news for AIIA and EB-5 investors, as it means that the current sustainment period — of two years following the first date of investment — remains active.

The different positions of either party, resulting in a disagreement, are as follows:

IIUSA’s Position: The case should be settled, under an agreement that would hold the case “in abeyance” while USCIS undertakes a new notice-and-comment process to determine the sustainment period. If USCIS fails to properly complete this process, IIUSA may reactivate the case to attack DHS for a breach of the settlement. The settlement would entail the revocation of USCIS’s interpretation of the post-RIA sustainment period, effective on the date of settlement.

Crucially, IIUSA calls for a new, two-tiered sustainment period for post-RIA investors. In the first tier, any EB-5 investors who invested before the settlement date would benefit from the current sustainment period (i.e., two years from the first date of the funds being invested). Those who invest after that settlement date, however, would be in the second tier, and would be subject to whatever new sustainment period USCIS reaches through its rulemaking process. Importantly, IIUSA has conceded that “a sustainment period tied to the period of conditional residence has become too burdensome for investors,” which is a view shared by AIIA. We hope that IIUSA honors this concession, and will at least try to avoid resurrecting harmful pre-RIA sustainment rules for post-RIA investors. Pre-RIA investors continue to be bound by pre-RIA sustainment rules, regarding which AIIA continues as a separate advocacy project.

DHS/USCIS’s Position: Any decisions regarding notice-and-comment rulemaking, and ipso facto this case, cannot be made at this time. The change in presidential administration, from that of Joseph R. Biden, Jr. to Donald J. Trump, means that USCIS is currently re-evaluating its policy priorities and strategic plans. Additionally, several appointments to senior positions at USCIS, including that of the Director, have not yet been made though there is news that Joe Edlow has been nominated to lead USCIS. These appointments are necessary for the aforementioned planning to occur.

Hence, DHS sought an additional 30 days to determine its position and, thereby, begin settlement negotiations with IIUSA, after which another JSR could be filed to apprise the court of the parties’ plans.

Upon receiving such a JSR, Judge Reyes ordered the parties to continue discussing the matter so as to reach total agreement on a settlement. She also ordered the parties to file a new JSR by or on March 21, 2025

AIIA’s Analysis and Response

Our objective at this time is to ensure as minimal a sustainment period for investors as possible (i.e., two years from the first date of the investment, as the RIA textually commands) in order to prevent any chance of redeployment whatsoever.

It is critical to note the absurdity of IIUSA’s position. Effectively, IIUSA is asking for two different definitions of the sustainment period to operate concurrently: a two-year period for post-RIA investors who invested before the settlement date, and an indefinite period for post-RIA investors that invest after the settlement date. This outcome, even if provisional, was clearly not intended by Congress when it wrote the RIA. AIIA firmly opposes IIUSA’s erroneous and burdensome request for a dual definition. Instead, we demand that the current two-year sustainment period continue for all EB-5 investments until the rulemaking process yields a new definition, if at all different.

It is a positive development that IIUSA has conceded, at the very least, that the current two-year sustainment period should apply to at least some investors. However, AIIA is deeply opposed to IIUSA’s pleading that any investments after that settlement be subject to a yet-undetermined sustainment period resulting from any rulemaking. Notice-and-comment rulemaking often takes several years to complete, and almost always invites litigation that prolongs uncertainty regarding the rule. Should IIUSA’s position be accepted, post-RIA investors after the settlement will be confronted with years long uncertainty about the period to sustain their investments. Likely, it will precipitate a decline in EB-5 investments. Hence, AIIA urges the EB-5 regional center body to concede that the current sustainment period should apply to all investments, including those made after the settlement, with any new definition taking effect for investments made only after the rulemaking is completed.

Furthermore, there is no guarantee that IIUSA will reach a settlement agreement with DHS as instructed by the Court. In such a case, Judge Reyes may issue a summary ruling and temporary injunction that reverts to the pre-RIA sustainment rule, which is the last operative definition whose validity was uncontested. Essentially the lack of agreement between both parties may lead to a reversion of the sustainment period to pre-RIA rules for all investors, including all post-RIA investors.

IIUSA may be seeking such an outcome, since the pre-RIA sustainment periods greatly benefitted regional centers due to visa bulletin backlogs and redeployment of funds, as aforementioned.

It is worth noting that recent political developments involving the EB-5 program, whereby the Trump Administration seeks to drastically modify it, have generated new challenges for the EB-5 community. Many EB-5 industry members have raised objections and some have even demanded that IIUSA unilaterally withdraw its claims. By maintaining its position, IIUSA is jeopardizing the existence of the EB-5 program for the cold self-interest of certain specific investment issuers. IIUSA’s demand to create an unknown sustainment period for investors that invest after their settlement date would harm the EB-5 market and jeopardize fundraising efforts for issuers across the board as they would now put forward investment offerings in front of investors not knowing when they can even repay their investors.

We will continue to monitor this case and strategize appropriately on how we should best proceed. Our legal efforts to defend investors will require your support. Litigation is expensive and, should AIIA intervene, we will be the only party challenging the EB-5 regional centers at the appellate level. Additionally, we intend to lobby any internal administrative process that may occur in going forward (e.g., notice-and-comment rulemaking). This effort, too, will require funds. To safeguard investor interests, please donate to this fundraiser today and share this blog with other members of the community.

Given the likelihood that notice-and-comment rulemaking will occur, AIIA is reserving for that process the use of any funds we have raised regarding this legal action. AIIA intends to submit a comprehensive comment during the rulemaking process that will legally compel USCIS to consider a definition that maximally benefits EB-5 investors.

However, should it be possible — especially if DHS takes a position that is contrary to the AIIA’s position — AIIA will seek to intervene in this case as a litigating party and challenge this case directly, by appealing to the United States Court of Appeals for the District of Columbia Circuit. As a litigating party, AIIA will incur significant legal fees, and another fundraising campaign will be necessary. We will soon update our members on the likelihood of such an outcome.

As always, your support is critical to AIIA’s efforts to fight on behalf of EB-5 investors. For this case, and for our other initiatives to defend investor interests, please consider donating to AIIA or joining our membership program to ensure our advocacy may continue.

Directory of Professionals

AIIA has curated a list of the top professionals from attorneys, investment specialists, to business plan writers to support all EB-5 stakeholders.

View Directory of Professionals

Leave your comments

Responses (1)

Directory of Professionals

AIIA has curated a list of the top professionals from attorneys, investment specialists, to business plan writers to support all EB-5 stakeholders.

View Directory of Professionals

Stay Up To Date With AIIA

Join our newsletter to stay up to date on EB-5 updates.

By subscribing you agree to with our Privacy Policy and provide consent to receive updates from our company.

Recommended Resources

How to find a good EB-5 Litigation Attorney

Choose an attorney with EB-5 and litigation experience who is organized, detail-oriented, and avoids making guarantees. You may need a...

Read More

The Redeployment Conundrum

Redeployment litigation arises when NCE managers reinvest EB-5 funds without proper judgment, exposing investors to unnecessary risk despite broad contractual...

Read More

“Privity” in EB-5 Litigation

EB-5 issuers often design complex structures and narrow “privity” relationships to make litigation difficult, forcing investors into uphill battles and...

Read MoreRecent Blog Posts

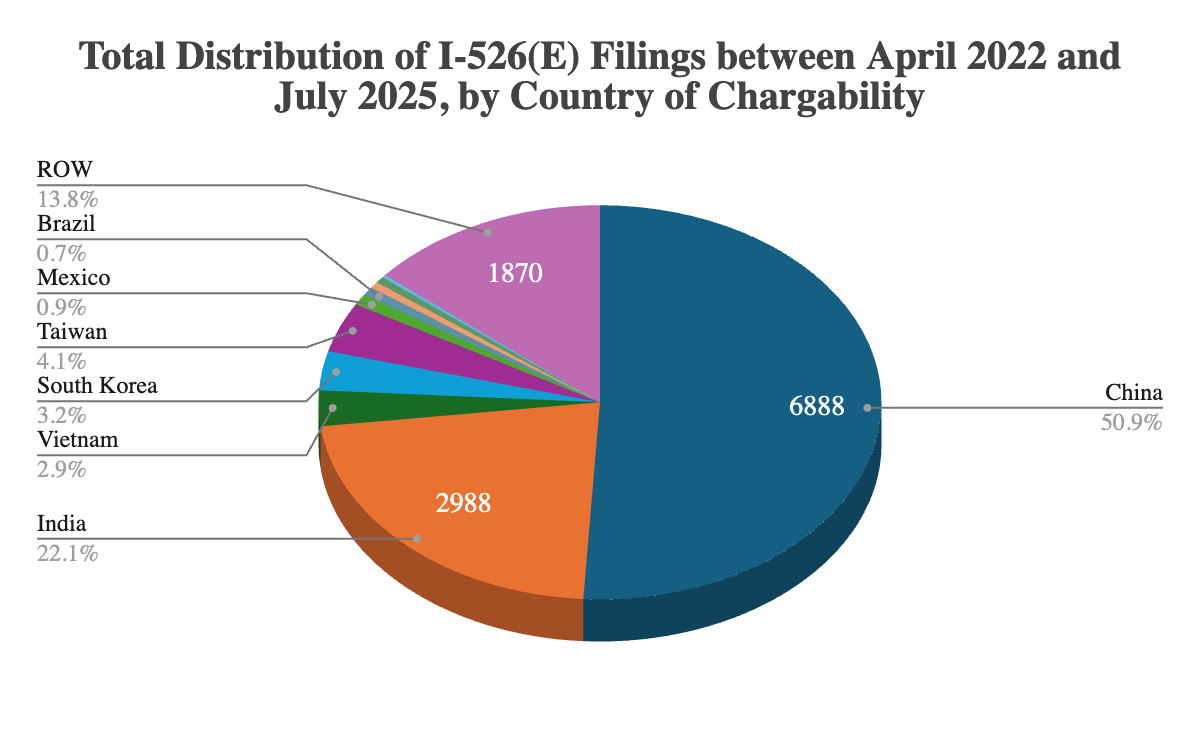

AIIA FOIA Series: Updated I-526E Inventory Statistics for July 2025

AIIA obtained new FOIA data through July 31, 2025 revealing how USCIS is actually processing EB-5 petitions, showing heavy prioritization...

Learn More

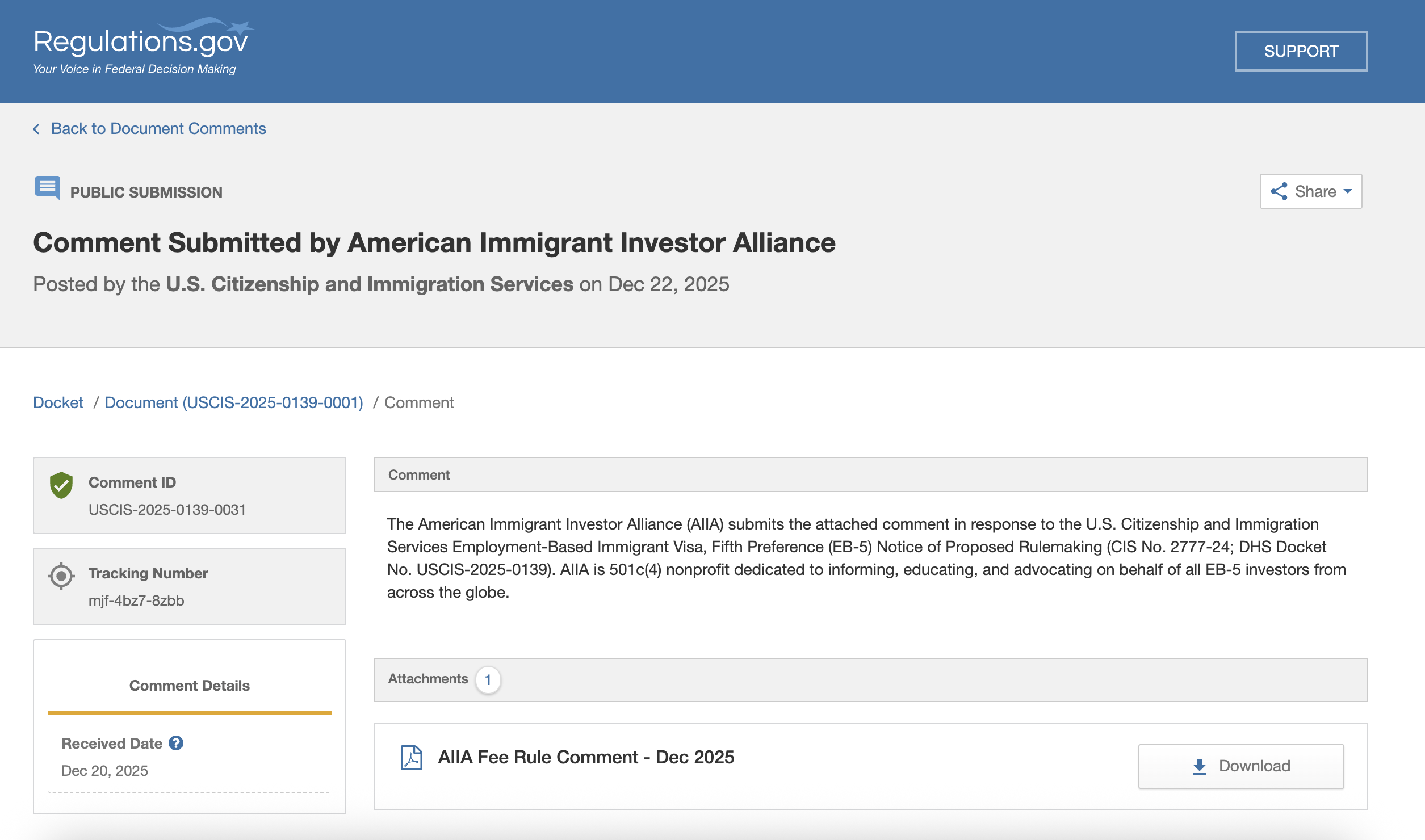

AIIA Submits Comments on USCIS NPRM on Updated EB-5 Fee Rule

AIIA submitted comments on USCIS’s October 2025 EB-5 fee NPRM supporting revised, lawful fee levels but urging refunds for overpaid...

Learn More

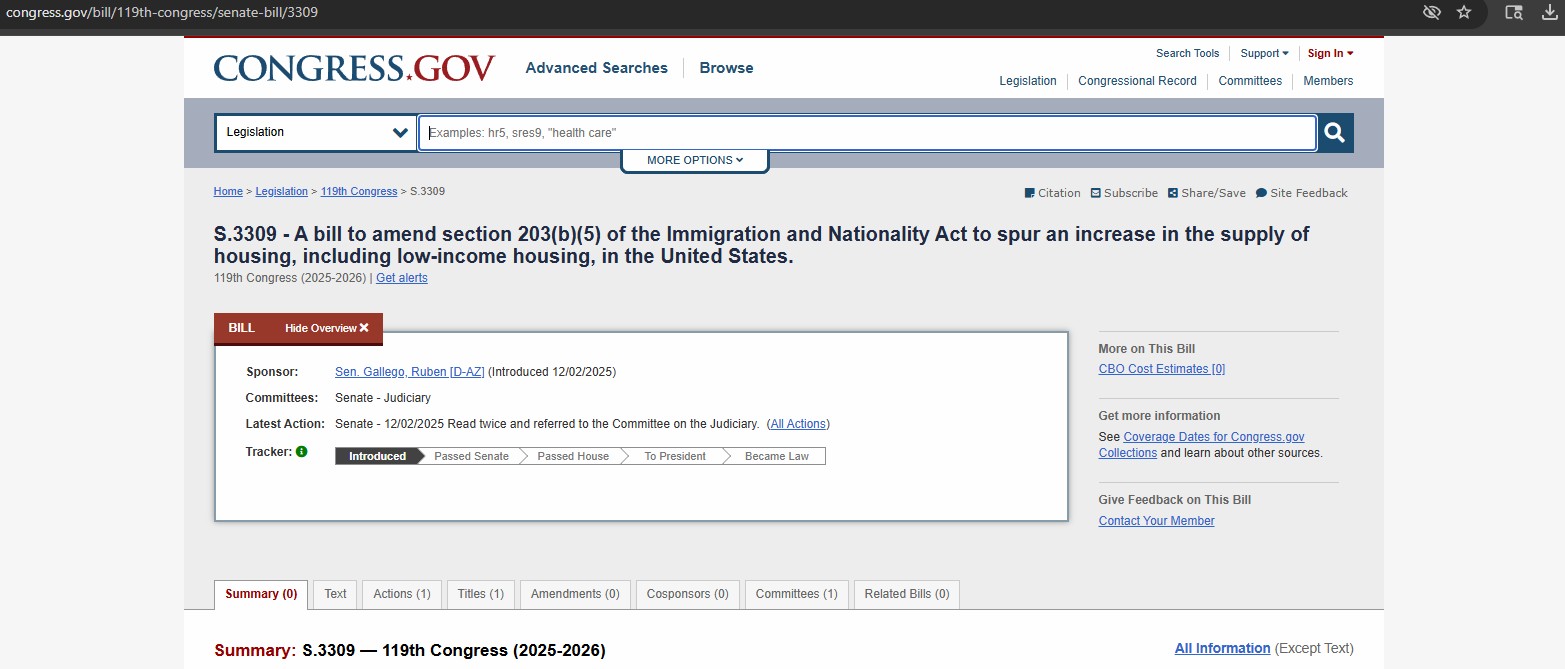

We Congratulate Senator Gallego for New Legislation that Leverages the EB-5 Program to Build Affordable Housing

Sen. Gallego's EB-5 bill mobilizes foreign capital to build affordable housing. This collaboration has boosted AIIA's Congressional ties & credibility...

Learn More

We Won The EB-5 Fee Increase Lawsuit

AIIA successfully won its lawsuit against USCIS’s April 2024 EB-5 fee increases, with a federal judge ruling that the agency...

Learn MoreGet In Touch With Us

If you have any questions, inquiries, or collaboration proposals, please don’t hesitate to reach out to us.

We are EB5 investors almost at the verge of filing for it. We are looking to get a little more clarity regarding this below statement:

`In the first tier, any EB-5 investors who invested before the settlement date would benefit from the current sustainment period` => Does this timeline considers the partial investments along with the filing of I-526 Petition only? Or this timeline states the full investment(800K) needs to be invested in the EB5 project (and not held by the Regional center before being invested)?